Reach Your Financial Goals With GoLoans

Read our expert financial guides. Compare rates and terms. Get the financial help you need today

What’s your financial goal?

Personal Loan Tips & News

Personal Finance Tips: Should I Use My 401(k) To Pay Off Debt?

25% of people between the ages of 24-35 have taken money out of their 401(k) retirement plan to pay down debt – and taking some money from your retirement savings to pay off your debt may seem like a good idea if you’re not sure how else to get out of debt.

Will COVID-19 Affect Personal Loans and Interest Rates?

Whether you’re looking to take out a personal loan of your own due to the spread of COVID-19 coronavirus, or you’re a financial services professional, you may be wondering how this pandemic has affected personal loans in America.

Personal Loans: Lenders Requiring More Personal Data on Loan Applications

For years your credit report data was enough for lenders to judge whether or not you are worthy of a personal loan. Recently, however, lenders have become hungry for what almost all companies want in 2020; more data.

Auto Loan Tips & News

Coronavirus is Affecting Auto Loans in a Big Way: Here’s Why

Interested in buying a new car? Wondering if now is a good time, or curious to learn more about how the COVID-19 coronavirus outbreak is affecting auto loans and car dealers? Let’s take a look now.

Subprime Auto Loans Could Be Driving the Next Financial Crisis

Will bad credit auto loans drive us into the next recession?

Auto Loan Interest Rates? Yep, They Just Hit a 22 Month Low

If the thought of buying a car makes you cringe, you will be happy to know that the average interest rate for auto loans decreased for the third month in a row in December 2019.

Home Loan Tips & News

Now Is the Perfect Time for Military Families to Refinance A Home Loan. Here’s Why

the Federal Reserve has been pressured to lower interest rates by the current administration to encourage continued momentum in our economy.

First Time Home Buyer Loans (How to Qualify)

Research, Compare and Apply for First Time Home Buyer Loans. Find Lenders With the Best Rates and Terms Online.

Feds Cut Interest Rates - Here’s How it Affects Mortgages in 2019

The Feds recently announced a 0.25% interest rate reduction on July 31st, 2019. It’s the first time the Feds have cut interest rates in over a decade.

Bad Credit Loan Tips

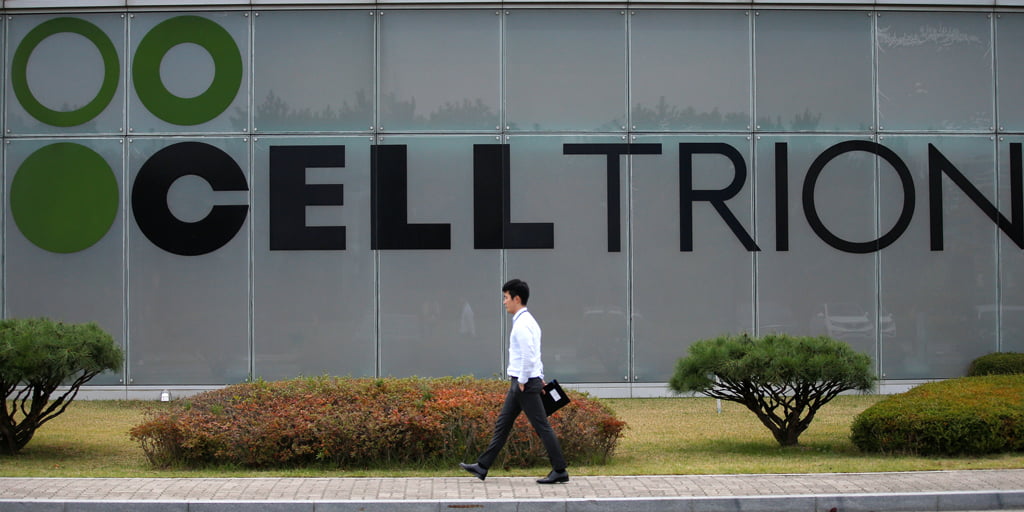

A South Korean Drugmaker Used To Borrow From Loan Sharks. He’s Now Worth $10 Billion.

Seo Jung-jin is a South Korean entrepreneur and the founder of Celltrion Inc., a South Korean drugmaker that is now working on developing a treatment for COVID-19 coronavirus

New Payday Loan Regulations Could Make Life Harder For Borrowers

The Consumer Financial Protection Bureau (CFPB) just repealed a set of rules and regulations that were put in place to protect payday loan borrowers

4 Reasons To Get An Installment Loan For Bad Credit Instead Of A Payday Loan

If you need some cash to cover an unexpected expense, you may be considering a payday loan. But even if you have bad credit, an installment loan such as a personal loan may be a better option.

Predatory Lending News

A South Korean Drugmaker Used To Borrow From Loan Sharks. He’s Now Worth $10 Billion.

Seo Jung-jin is a South Korean entrepreneur and the founder of Celltrion Inc., a South Korean drugmaker that is now working on developing a treatment for COVID-19 coronavirus

What is a Loan Shark?

A Loan Shark is a Predatory, Unlicensed Moneylender That Takes Advantage of People With Poor Credit. Read More Here >

Loan Sharks Online: How to Find an Alternative Loan With Bad Credit

Need a loan shark for a bad credit loan? Here’s how to find a fast loan